The Green Sheet Online Edition

November 26, 2012 • 12:11:02

Opportunities in RAN and private-label programs

The restricted authorization network (RAN) concept is used primarily for programs outside or in between the traditional closed-loop and network-branded, open-loop programs. A RAN, as classified by the networks, is used for building a restricted participating network of merchants where a payment card is used without any change at the acquiring side.

This is intriguing, and yet, is almost underplayed by the networks, as it is counterproductive to their brands. The "restricted" nature of a RAN program almost mandates the removal of the network logo from the payment instrument because it is not universally accepted where the network brand is.

The RAN appeal

In my career as a payment systems consultant, I have come across various merchants (primarily midsize to small) interested in using the RAN concept, but because of the lack of awareness and availability of program managers, they have found the option difficult to implement.

I discuss the possible variants to RAN in this article. I believe they might have greater value in the world of payment acquiring, especially with the pervasiveness of social media and mobile technology and their increasing influence on payments.

I am not sure how to define the variants because, clearly, they are not RAN as originally understood. Some people call them restricted- or limited-loop, private-label card programs. I have also heard them referred to as controlled participating networks.

RAN traditionally was used, for example, in single- and multi-retailer environments, shopping mall card programs, employee and government benefit programs, travel and entertainment card programs, and merchant funded discount networks.

Network control

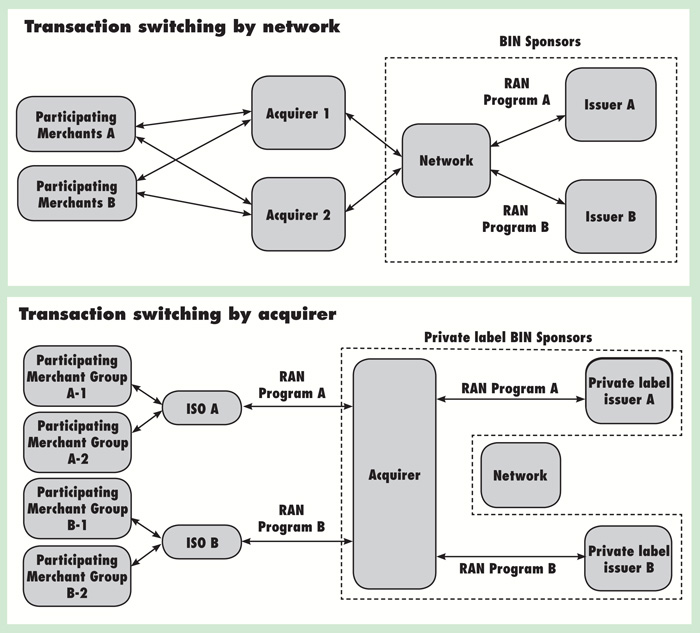

Typically, in RAN environments a transaction is switched by the networks to the appropriate issuer, as the network remains in control. For example: Issuer A has a Visa Inc. RAN program running for a select set of participating merchants. Without making changes to the POS environment, these merchants could accept the cards.

A transaction would flow the same way as a credit or debit transaction from the POS to the acquiring processor to the network (in this case Visa) where it would be switched to Issuer A for authorization. Issuer A knows if it has come from a participating merchant, and bingo, the transaction is approved.

If the RAN card is used at a nonparticipating merchant location the transaction is denied. Works like a charm. (See the accompanying chart titled "Transaction switching by network" for a depiction of this type of transaction flow.)

A possible variation of this is what is happening in the recent deal between PayPal Inc. and Discover Financial Services. PayPal-issued prepaid/debit cards will be riding the Discover rails.

It is not clear yet whether PayPal will be accepted by default at all Discover merchant locations or whether acceptance will be restricted to certain locations PayPal selects.

A player like PayPal could pull off a deal with Discover, but what about smaller players who want to run private programs? Their choice was easy if it was a traditional single retailer closed-loop program or, on the other hand, an open-loop program.

Processor control

However, there is merit in technologically considering using switching and authorization at the processor level rather than the network, and passing the program features right down to the ISO level, which can create custom programs for their smaller merchants.

As an example, if the acquiring processor gets a bank identification (BIN) number range for a prepaid program from an issuer and then runs a program for its ISOs, thereby enabling them to create mini restricted networks under them as needed to serve their merchant base, it would add significant value and increase the portfolio of services an ISO could provide to its targeted retailers.

No POS change would be needed, as ISOs typically have a one-to-one relationship with their acquirers, and all transactions would then switch for authorization at the processor level. Network participation is almost negated. (See the accompanying chart titled "Transaction switching by acquirer" for a depiction of this type of transaction flow.)

Added value

The payments industry is changing dramatically, and the acquiring channel is focused on making its services and programs relevant to merchants. These restricted networks could add value beyond payments; coupling them with promotions and loyalty could be a good way for acquirers to increase stickiness.

Reduced credit availability, coupled with increased adoption of newer technologies like mobile and social media platforms, could result in targeted and relevant value-added prepaid programs for merchants and consumers.

Strong use of consumer data and promotions could make some of these private-label and restricted-loop programs effective and profitable for all participants.

Some leading processors are running such programs for their ISO channels. Technologically, it is possible to do; from a business sense each use case will have to be vetted and tailored for the target market.

Mustafa Shehabi is the co-founder of PayCube Inc., a San Francisco Bay Area-based payment consulting and IT services company providing custom software solutions and custom gateways for acquirers, ISOs, retailers and varied organizations in the world of payments and consumer transactions, including prepaid and gift card program, loyalty and promotion, payment startup, POS solution, mobile payment and e-commerce players. PayCube uses a blend of on-site and offshore delivery capabilities, with a staff of retail and payment-focused software engineers, systems architects, project managers, tech leads and systems analysts. For more information, email ms@paycubeinc.com, call 925-285-6265 or visit www.paycubeinc.com.

Notice to readers: These are archived articles. Contact information, links and other details may be out of date. We regret any inconvenience.