The Green Sheet Online Edition

July 9, 2012 • 12:07:01

Lead sources - the front line in sales competition

The acquiring industry is nothing if not dynamic. And though much of the time this leads to upside opportunity, it would be a mistake to ignore the mounting signs of maturation of the business.

Though "margin" events like the Durbin Amendment to the Dodd-Frank Act of 2010 will keep earnings buoyant for some time to come for most acquirers, the writing is on the wall that competition will become gradually more intense.

Decline in productivity

One of the arenas in which this rise in competitive intensity is apparent is demonstrated by the increase in pressure on traditional sales models, as well as the substantial decline in sales productivity rates from the first half to the back half of the last decade.

Indeed, as part of our ongoing research, our firm measures new merchant sales per full-time equivalent employee per month; we found that from 2000 to 2011 the annual change in that figure was in decline:

- Field sales.......................................-9 percent

- Telesales.........................................-3 percent

This decline in productivity reflects a raw increase in sales staff and related investment from acquirers intending to maintain the growth rates to which they have become accustomed, though in an environment where same-store growth is in secular (long-term) decline.

In addition to putting pressure on the growth equation for many acquirers, declining sales productivity has become a substantial financial issue for some. Whereas virtually every aspect of the value chain has been subject to declining unit costs, acquisition costs remain stubbornly high and rising, resisting scale economies or improved efficiency.

Quality and quantity leads

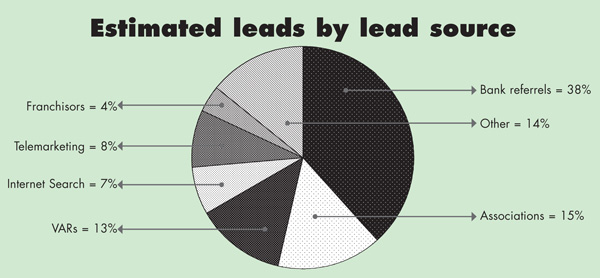

If a management team could take only one action to improve sales productivity, that action would be improving the quality and quantity of the leads the sales force has available to it. There is a huge amount of experimentation in lead generation in acquiring, ranging from the use of comparison websites on the Internet to the use of nontraditional partners such as insurance agents and wholesalers.

However, it is still true that the majority of leads come from a relatively narrow set of categories, as estimated in the chart, titled "Estimated leads by lead source," accompanying this article.

In recent years, competition to sign the traditional lead sources has increased substantially. For example, the large bank market is highly competitive, and new partnerships in this market are somewhat uncommon.

Very few large banks change providers once in an alliance of some sort with an acquirer. Of the current top 20 banks, only three have changed acquirers; and in each case, those three had special circumstances often related to broader mergers and acquisitions of the parent company.

By contrast, the association's business is highly fragmented, with no single dominant acquirer and less than complete penetration. The value-added reseller (VAR) market, too, has extremely competitive pockets, but overall is not fully penetrated and lacks a single dominant player.

There is much evidence of acquirers specializing around lead source. For example, the players most focused on organic Internet searches are different organizations with different skill sets (search optimization, etc.) than those acquirers pursuing paid search.

The set of acquirers focused on community banks is different than the acquirers focused on national and super-regional banks (and the underlying bank needs and economics are different). An acquirer committed to the VAR channel generally has different capabilities and organization than other types of acquirers.

Sub-segmenting lead sources

In short, competition for these lead sources has its own set of dynamics and requirements - selling through a bank franchise referral partner bears little resemblance to selling effectively through associations.

Whereas specialization around sales channel and merchant segment has become conventional wisdom in acquiring, specialization around lead source is taking the same path and level of importance.

The challenge for acquirers is not solely to identify the main lead source or sources that will drive the acquirer's business, but also to sub-segment the lead source category and to develop competitive advantage in sourcing and managing a given lead source.

(So, it's not simply associations but rather associations that are member service-oriented, regional or local, and targeting business-to-business members, for example.)Of course, it is a bit of a false choice to focus on solely one tactic to improve sales productivity, as sales management from recruiting to training to compensation has a substantial impact, as does pricing strategy and product management.

Nevertheless, a high performance and differentiated lead source will hide a lot of sins in a sales organization, and lead source management is quickly becoming the front line in the sales productivity arms race the industry has been experiencing for some time.

Notice to readers: These are archived articles. Contact information, links and other details may be out of date. We regret any inconvenience.