The Green Sheet Online Edition

June 11, 2012 • 12:06:01

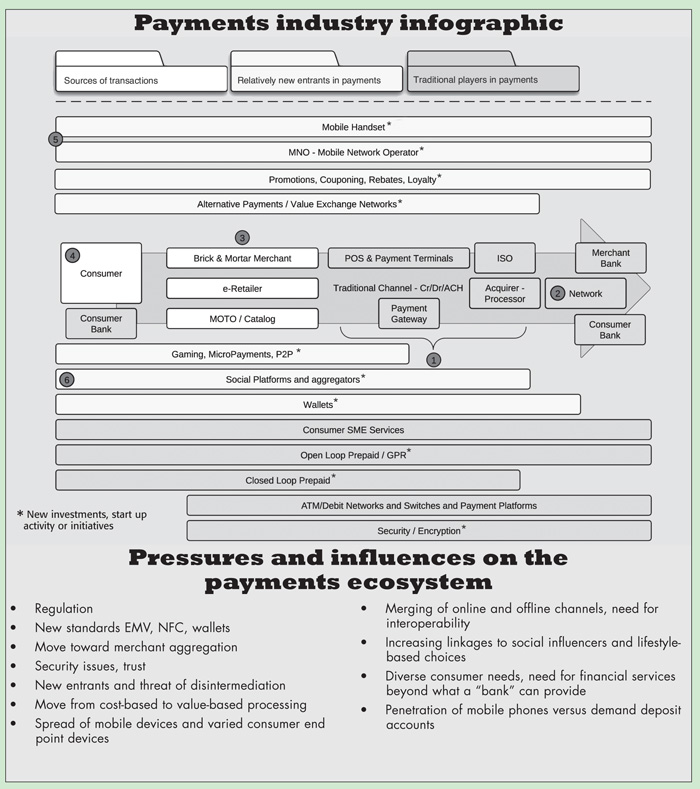

Payments industry infographic

Acquirers

Acquirers

As the payments industry moves from issuer-centric to acquirer-centric (from players who own the customer running the network to players who own the merchant running the network), acquiring roles are beginning to overlap. Traditional hardware and POS players are getting into the online world, offering their own gateways, and traditional gateway players are trying to get into the POS world.

This space is also beginning to view transactions differently as the debate of transaction aggregation versus merchant aggregation matures This segment is rich in transaction data and is likely to use this to create differentiation. Acquirers will continue to play a key role in shepherding payment transactions; they will need to adapt their acquiring infrastructures to address the unique needs of their merchants.

Networks

Networks

The payment networks (Visa, MasterCard, AmEx, Discover), which have traditionally been escrow agents of sorts on behalf of the issuers are now active participants in the acquiring play. As the acquiring game gets aggressive and creative, the networks are bulking capabilities in the online and offline world, through strategic investments in companies and building internal capabilities to shore up their offerings to tackle new and emerging players like the mobile network operators (MNOs), wallets, closed-loop person-to-person (P2P) networks, etc.

Time will tell how much the payments market will migrate outside of bank-based instruments. This will be the single biggest factor impacting the role of the networks. The networks today bring reach, trust and branding, which is hard to beat.

Retailers

Retailers

Future payment battles will be fought and won here. The fragmentation of retail and how these segments are addressed is going to define what the future face of payments looks like. Influences from market players in search, transactions, social media, mobile, loyalty and promotions are creating segments in retail outside of traditional brick-and-mortar and e-tailers, we are seeing the emergence of various P2P portals, web stores, app stores, carrier billing and value exchange networks. The key challenge is to build cross-platform infrastructures to engage, influence and induce repeatable buying behavior in consumers.

Consumers

Consumers

If retail is the "egg," the consumer is the "chicken" in the chicken-and-egg situation the world of payments finds itself in. Technology standardization, which is key for mass adoption, will happen only if the consumer is linked effectively to the retailer. Almost all the innovation that we are seeing from a plethora of vendors is for this sole purpose, and rightly so.

As the retail space is getting increasingly fragmented, the advent of technology and consumer lifestyle changes like the access to fundamental banking/financial services is driving segmentation within the consumer base. The consumer needs solutions and technologies that provide value greater than the friction they produce. Aspirations and lifestyle-based interactions are what today's consumer is looking for.

MNOs

MNOs

The MNOs are the single biggest strategic threat to the traditional payment networks. They are omnipresent globally and bring deep consumer relationships and trust - add to that the growing global adoption of mobile phones.

Mobile payments and the role the MNOs play will depend on the economics and their involvement in the transactions. Near field communication (NFC) and Europay/MasterCard/Visa (EMV) and their adoption will also have an impact.

MNOs will need to realize that consumers are/will view a mobile phone as a channel to use services and not the only medium to interact. Hence, for mobile payments to succeed, the technology will have to be seamless and interoperable, as in, it will have to almost be magical to fade in and fade out as the use case transpires.

Social platforms

Social platforms

Acquirers bring transactional intelligence to the ecosystem, traditional gateways bring consumer purchasing intelligence, search engines bring search intelligence, social platforms that want to participate in the payments ecosystem will have to bring "social relationship intelligence," which can be effectively monetized.

If you think about various kinds of transactions which ride the payments rail today (generic payments, prepaid/gift, loyalty, promotions, couponing, value exchange, micropayments, P2P, etc.) all of them can be influenced through some kind of social framework.

Social platforms have the potential to go far beyond the last leg (payments) and into influencing consumer retail behavior and adoption.

Editorial Note: This article was first published in the March 30, 2012, issue of Merchant Service Times. Reprinted with permission. All rights reserved; This was adapted from the PayCube Inc. Payments Industry Infographic, © 2012 PayCube. All rights reserved. Adapted with permission. For more information, contact Mustafa Shehabi at ms@paycubeinc.com, or visit www.paycubeinc.com.

Notice to readers: These are archived articles. Contact information, links and other details may be out of date. We regret any inconvenience.