The Green Sheet Online Edition

April 4, 2025 • 25:04:02

Empowering SMB growth through digital lending

In the United States, small and midsize businesses (SMBs) form the foundation of local economies and play a key role in the broader U.S. economic landscape. The last quarter of 2024 saw a surge in optimism among small business owners that continued into the new year.

However, this optimism is now being tempered by emerging economic disruptions that are increasing levels of uncertainty.

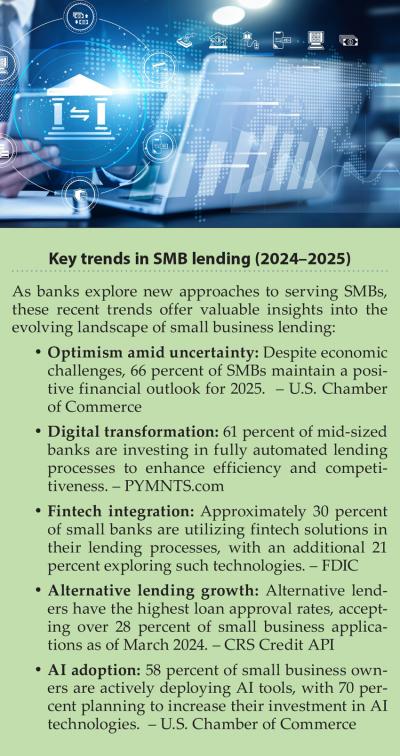

Despite this, U.S. Chamber of Commerce data indicates that two-thirds of SMBs continue to hold a positive attitude about their financial outlook for 2025 and that 58 percent reported capital outlays in the last six months with 19 percent planning capital purchases in the next three months alone (see www.uschamber.com/small-business/small-business-weekly-forecast).

For SMBs, unlocking liquidity is vital for achieving growth and can be accomplished through increasing profit margins, improving inventory management and securing working capital financing.

Banks with the right solutions in place can position themselves to help SMBs access the capital required to grow, while establishing long-term relationships that can endure – even in times of uncertainty.

How banks can best serve SMB customers

Timing is a critical factor for small businesses, and despite the trillion-dollar market for business financing, many SMBs struggle with obtaining timely access to capital. While inflationary and new tariff concerns persist, the prospect of lower interest rates has fueled some levels of confidence among business owners.

Capitalizing on emerging opportunities requires seamless and swift access to funding. Fintech firms and many financial institutions are already integrating automation into the SMB lending process to accelerate decision-making and disbursement.

Additionally, investing in their own digital lending infrastructure or forming strategic partnerships with leading lending-as-a-service (LaaS) fintech providers enables banks to maintain an edge in a hyper-competitive market.

Enhancing scalability and efficiency in SMB lending

Many banks continue to tread cautiously when it comes to expanding their SMB lending efforts due to perceived risk and operational complexities. Typically, SMB lending has been associated with high origination costs and inefficient manual processes that make scalability difficult. Tackling these challenges can be accomplished by leveraging data-driven automation that reduces costs, mitigates risk and enhances the borrower's experience.

Banks possess large volumes of existing customer data that is often an underutilized asset in streamlining SMB lending. This is largely due to fragmented and outdated systems compounded by siloed customer data that hinder banks from creating a holistic view of their customer relationships.

The absence of a modernized data infrastructure and real-time analytics causes operational hurdles that slow down processing and frustrate business owners.

It is critical for banks to move away from traditional manual approaches for loan decisioning. Identity profiles for small business customers are multi-faceted, so looking beyond traditional data sources to form a 360-degree view of small business identity becomes a critical factor for streamlining a successful SMB lending program.

Leveraging AI-driven risk models enables banks to better evaluate risk, detect fraud and speed up decision-making.

By embracing an integrated approach to data analytics and insights, banks can expand their SMB customer base without taking unnecessary risks. AI-powered models can provide a more accurate assessment of borrower creditworthiness while boosting operational efficiencies.

Expanding Lending Opportunities

Frequently, loan applications do not meet a bank's internal lending criteria, and banks are unable to find a financing offer for these small businesses. As a result, banks tend to miss out on an additional revenue stream in the form of non-interest income.

This is avoidable through partnering with an established funding network, which allows banks to provide additional lending options while enhancing their valuable customer relationships.

Instead of turning away SMB borrowers who fall outside existing credit requirements, banks' applicants are referred to an external funding network to receive the financial support they seek while the bank generates referral income.

As an example, banks ranging from $1 billion to $5 billion in assets can realize an additional 8 percent to 20 percent in non-interest revenue annually. Integrating with an established funding network allows banks to further expand their SMB financing offers allowing SMB borrowers access to alternative financing options without losing them to competitors.

Other key considerations for banks adopting data-driven lending strategies

In addition to a trusted network of alternative funders, banks can also implement modernized SMB lending solutions. Banks should ensure their technology investments support the following capabilities:

- Enhancing competitiveness: Provide SMB borrowers with seamless, fully digital lending experience that matches or surpasses fintech and large bank offerings.

- Automating and accelerating loan processing: Streamline application intake, decisioning and approvals through integrated Know Your Customer (KYC), Know Your Business (KYB) and credit scoring solutions.

- Leveraging data insights: High-quality, unified data enhances both the speed and accuracy of lending decisions, providing a more holistic view of applicants.

- Optimizing portfolio performance: Automated portfolio monitoring enables banks to track SMB loan performance, proactively identify potential risks and reduce default rates.

Amid rising uncertainty, small businesses continue to show resilience. Ultimately, SMB customers will choose to partner with banks that provide the tools and services needed to maintain their operations and foster growth. It's imperative that banks equip themselves with modern loan origination capabilities that meet their current and future customers' financing needs.

Will Tumulty serves as CEO of Rapid Finance, a Bethesda, Md.-based fintech and provider of working capital to small businesses in the United States. Contact him via LinkedIn at linkedin.com/in/will-tumulty-15a6462.

Notice to readers: These are archived articles. Contact information, links and other details may be out of date. We regret any inconvenience.